Image by TheTruthAbout via Flickr

Image by TheTruthAbout via Flickr

When deciding whether or not to refinance there are a number of things to consider. These include things like: how long you plan to stay in the house, how much cash you have available for closing costs, and how much lower your new interest rate will be.

But most people, including me, want a simple straight forward bottom line analysis that indicates: is it worth it or not?

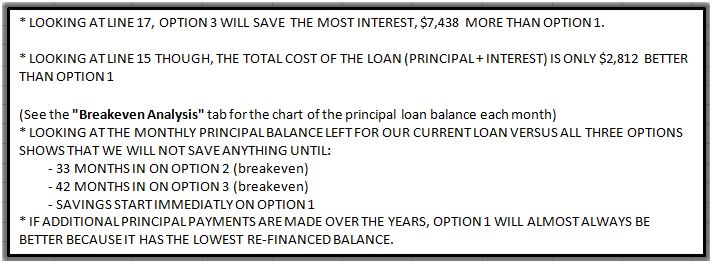

The answer here is a comprehensive breakeven analysis. This analysis looks at payback time based on the principal balance not only on the payback for the closing costs.

The main reason is that just looking at the payback of the closing costs is not the best way to reveal the overall costs associated with refinancing a loan, which means restarting your loan repayment schedule of payments (amortization table).

The best way to see this is to plot out the principal balance each month over the life of the loan for your current loan versus each of the options that you are considering.

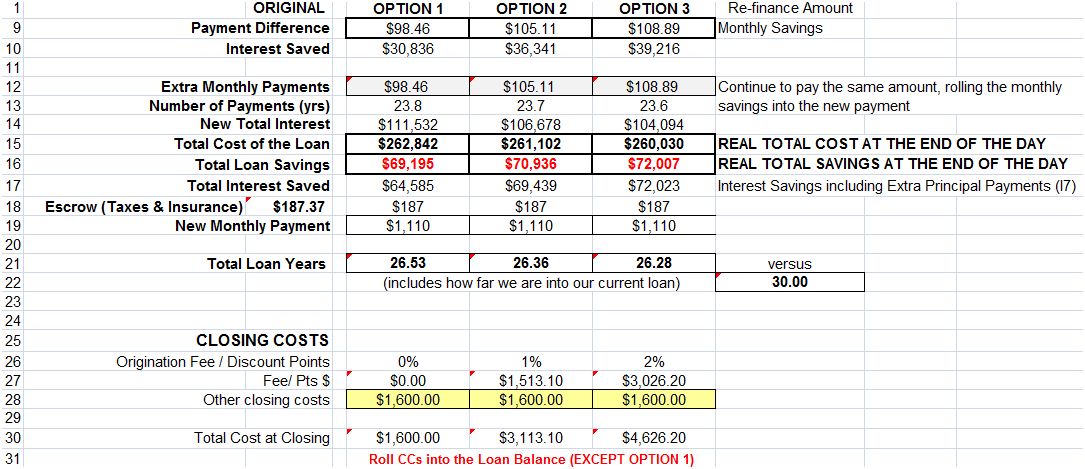

For my analysis we had 3 options and we needed to roll most of the closing costs into the loan because we decided that we wouldn’t use our emergency fund to refinance. We also determined that what ever savings we achieved on the monthly payment we would just roll it in and continue paying the same amount as our original payment.

Building each of these things in to excel I created the amortization tables for all 4 situations (original plus 3 options). I then plotted the monthly principal balance over the life of the loans. This graph clearly shows the real breakeven point for each of the options. As in, how many months from now will the refinance options begin to have a lower principal balance than the original loan. This is the TRUE breakeven point.

Below are some screen shots from my personal spreadsheet analysis. Click images to enlarge.

If there is enough demand I could make the spreadsheet available for download.

Options:

Option Details:

Notes & Explanations:

Breakeven Analysis Graph:

RSS Feed

RSS Feed Email Subscription

Email Subscription

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_c.png?x-id=dee50ffd-5cfc-4558-9dde-0c9d2e2925ca)

Why not also create a what-if scenario based on the three here but if you sold in 3 years? That may change your approach a bit.

I refinanced 3 times, each time with no point, no closing, and paid slightly higher rate, but didn't worry about the expense. I see your scenarios include financing the closing costs. Slippery slope.

This is very interesting. I will be taking a detailed look. I appreciate the level of detail although I cannot (yet) say that I agree totally with your premise of what defines "break even". People refi for different reasons and what satisfies their needs may not be the same as yours. However, I really like what I've read and plan to review in greater detail.

Separately, I just wrote a blog post called, "How to Compare Rates for Mortgage Refinancing" at http://www.finestexpert.com/blog/index.php/2010/06/how-to-compare-rates-for-mortgage-refinancing/

The key premise is that you cannot simply go by interest rate or APR, but must instead consider the length of time you intend to hold onto the mortgage.